Struggling with managing finances in construction projects? Construction accounting methods can offer a powerful solution where traditional methods fall short. Addressing the unique financial challenges of the construction industry, construction accounting provides best practices to maintain financial health and ensure project success. Let’s navigate these complexities together!

Table of Contents

- Understand the Fundamentals of Construction Accounting

- Challenges in Construction Accounting

- Best Practices in Construction Accounting

- Construction Accounting FAQs

Understand the Fundamentals of Construction Accounting

Construction projects stand out from other business ventures. They’re typically long-term endeavors, requiring significant financial investment, extensive resources, and intricate contracts. To navigate these complexities, construction companies rely on specialized accounting practices. Here are some key aspects that differentiate construction accounting:

- Job Costing in Focus:Every expense incurred needs to be meticulously tracked and linked to specific projects. This includes direct costs (materials, labor, equipment rentals), indirect costs (overhead expenses), and any retention holdbacks. By meticulously documenting these costs, construction companies can accurately assess the profitability of each project.

- Percentage of Completion Method: Unlike some accounting methods that recognize revenue only upon completion, construction accounting often utilizes the percentage of completion method. This method recognizes revenue and expenses proportionally to the amount of work finished by the end of an accounting period. This provides a more realistic picture of a project’s financial health as it progresses.

- Retention Tracking: Construction contracts frequently involve retention clauses. This means a portion of the payment is withheld until the project’s completion or until specific milestones are achieved. Retention tracking ensures quality work and project completion by incentivizing contractors to meet these benchmarks.

Challenges in Construction Accounting

Managing finances in the construction sector presents unique challenges compared to more conventional accounting fields. Here are some of the most common hurdles faced by construction companies:

- Project-Based Work: With distinct projects rather than continuous sales, tracking income and expenses is complicated in construction.

- Long Contract Cycles: The extended duration of projects complicates revenue recognition, as earnings are often tied to specific milestones.

- Cost Overruns: Unpredictable issues such as material price fluctuations or labor shortages can lead to cost overruns, impacting the budget significantly.

- Change Orders: Project scopes can change, requiring budget and contract adjustments. Efficient management of these changes is vital to maintain profitability.

- Overhead Complexities: Proper allocation of overhead costs to specific projects is challenging but necessary for accurate job costing.

- Manual Processes: Manually entering data and keeping time can result in errors and inefficiencies, hampering overall financial management.

These challenges can lead to inaccurate financial reporting, difficulty in securing financing, and missed opportunities for maximizing profitability. By implementing best practices and leveraging construction accounting software, companies can overcome these hurdles and achieve greater financial control.

Best Practices in Construction Accounting

To manage the financial complexities of construction projects, companies should adopt the following best practices:

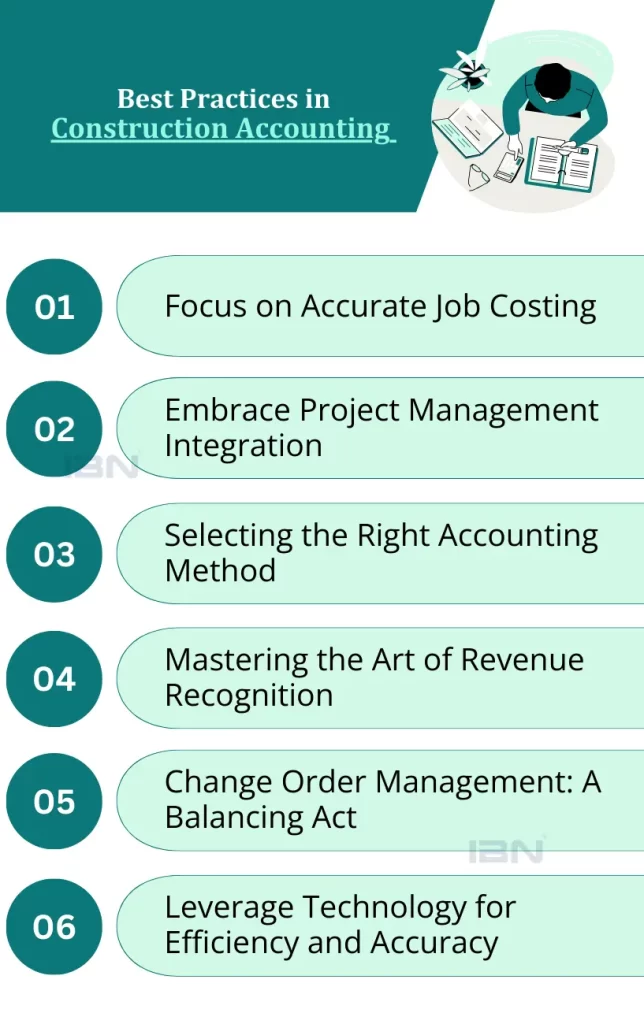

1. Focus on Accurate Job Costing

In the realm of construction, every project represents essentially a distinct business endeavor. Accurately assessing the cost of each project is crucial to grasping its profitability. Job costing, a fundamental aspect of construction financial management, diligently monitors all direct and indirect expenses linked to a particular project.

- Direct Costs: These are expenses directly tied to a particular project, such as materials, labor, and equipment rentals.

- Indirect Costs: Often referred to as overhead, these encompass broader company-wide expenses that indirectly support projects, like salaries for administrative staff, utilities, and insurance.

Effective job costing requires a well-defined system for capturing and allocating these costs. Construction accounting software can be a valuable tool in automating these processes and generating detailed reports that provide a clear picture of project profitability.

By closely monitoring job costs, you can:

- Identify areas for cost optimization.

- Set realistic project budgets.

- Negotiate contracts with a clear understanding of profit margins.

- Make informed decisions about change orders (discussed later).

2. Embrace Project Management Integration

Construction projects involve a multitude of moving parts, from material procurement and labor scheduling to subcontractor management and progress billing. Integrating your accounting software with your project management system can streamline workflows and enhance financial visibility.

This integration allows you to:

- Automatically capture project-related costs from purchase orders, timesheets, and subcontractor invoices.

- Track project progress and compare actual costs to budgeted costs in real-time.

- Generate reports that provide insights into project performance and identify potential cost overruns.

3. Selecting the Right Accounting Method

One size does not fit all when it comes to accounting methods in construction. The choice between cash-basis accounting and accrual-basis accounting depends on the size and complexity of your business:

- Cash-Basis Accounting: This simpler method records income when cash is received and expenses when cash is paid. It’s suitable for smaller companies with straightforward projects.

- Accrual-Basis Accounting: This method recognizes income when it is earned (even if not received yet) and expenses when they are incurred (even if not paid yet). This method is required for larger companies and those working on long-term projects, as it provides a more accurate picture of financial performance.

4. Mastering the Art of Revenue Recognition

Revenue recognition, the process of recording income when it is earned, presents unique challenges in construction due to the extended project lifecycles and progress payments. Here are the three primary revenue recognition methods used in construction:

- Percentage of Completion: This method recognizes revenue based on the percentage of work completed on a project at the end of each accounting period. It’s suitable for long-term projects with clearly defined milestones.

- Completed Contract Method: Revenue is recognized only upon full completion and acceptance of the project. This method is often used for smaller projects or those with high upfront costs.

- Cash Receipts Method: This method recognizes revenue only when cash is received from the customer. While simpler, it may not provide a clear picture of your company’s financial performance.

Choosing the appropriate revenue recognition method depends on the nature of your projects, contract terms, and the desired level of financial transparency. Consulting with a qualified accountant can help you navigate these complexities.

5. Change Order Management: A Balancing Act

Change orders, and modifications to the original project scope, are inevitable in construction. While they can present opportunities for additional revenue, they can also disrupt budgets and timelines. Effective change order management is crucial for maintaining project profitability.

Here are some best practices for managing change orders:

- Make sure that all changes are documented in writing, including the scope of work, costs, and approval process.

- Negotiate fair pricing for additional work.

- Update project budgets and timelines to reflect the impact of the change order.

- Communicate the changes effectively to all stakeholders.

By implementing a robust change order management system, you can mitigate risks and ensure that changes contribute to, rather than detract from, your project’s success.

6. Leverage Technology for Efficiency and Accuracy

Construction accounting software is not a luxury; it’s a necessity. These specialized software solutions offer a range of functionalities designed to streamline processes, improve accuracy, and enhance financial visibility. Here’s how accounting software can empower your business:

- Automated Workflows: Eliminate manual data entry by automating tasks such as generating invoices, processing payments, and reconciling bank statements. This reduces the risk of errors and frees up valuable time for strategic tasks.

- Improved Collaboration: Foster collaboration between accounting, project management, and field teams by providing a centralized platform for accessing and sharing financial data. This promotes better communication and decision-making.

- Enhanced Reporting: Generate real-time reports that provide insights into project performance, job costing, cash flow, and overall financial health. Use these reports to identify trends, make informed decisions, and improve profitability.

- Mobile Accessibility: Access project financials and reports from anywhere, anytime with mobile-friendly accounting software. This allows for on-site cost tracking and real-time decision-making.

7. Embrace Internal Controls and Security

Construction companies are susceptible to various financial risks, including fraud, theft, and errors. Implementing strong internal controls is crucial for safeguarding your financial assets. Here are some key areas to focus on:

- Segregation of Duties: Ensure no single employee has control over multiple critical financial processes, such as approving invoices and making payments. This helps prevent unauthorized activities.

- Access Controls: Restrict access to financial data and systems based on job roles and responsibilities.

- Regular Reviews and Reconciliations: Regularly review bank statements, accounts payable and receivable, and project budgets to identify discrepancies and potential errors.

- Data Security: Implement robust data security measures, including strong passwords, encryption, and regular backups to protect sensitive financial information.

8. Build Strategic Partnerships with Financial Professionals

Partnering with an expert accountant is a great way to ensure robust financial management. The expertise of construction accounting and financial management professionals at IBN Technologies, combined with sophisticated accounting software, results in an effective synergy. This collaboration empowers you to:

- Make informed decisions rooted in precise and insightful financial data.

- Boost your profitability by refining job costing and enhancing project management.

- Reduce risk with robust internal controls and expert compliance advice.

- Concentrate on what you do best—building excellence—while IBN handles the intricate financial details.

With IBN Technologies by your side, you gain a trusted financial partner who equips you to tackle the challenges of the ever-changing construction industry confidently and lays a strong foundation for enduring success.

Contact us to schedule your consultation and start building a more profitable and secure future!

Construction Accounting FAQs

- Q.1 Is construction accounting different?

- Yes, construction accounting differs from general accounting as it specifically deals with the complexities of project-based financial management in the construction industry.

- Q.2 What type of accounting is used in construction?

- Construction companies commonly use job costing to track expenses directly or indirectly associated with specific projects, and they often employ the percentage of completion method for revenue recognition.

- Q.3 Which method of accounting is best for a construction company?

- The percentage of completion method is typically best for construction companies. It matches revenue recognition with project progress, offering a more accurate financial view throughout the project’s duration.